|

|

|

|

|

|

| Your retirement plan allows you to borrow from your account and pay back the loan over time. In effect, you actually use your own retirement savings as collateral for the loan. |

|

|

| All plans have loan policies, including minimum and maximum amounts you can borrow, circumstances under which you can borrow, possible fees, and the interest rate you'll pay. When you take a plan loan you are signing a legally binding agreement. Like any contract, it's best to read your plan's loan policies and consider all your options before you sign anything. |

|

| Considerations |

|

|

|

|

A loan from your retirement account can provide you with a source of immediate cash if you need it. |

|

|

You don't need to "qualify" for a loan from your account, like you would if you applied for a bank loan. Having vested money in your account is qualification enough. |

|

|

When you borrow from a bank, you repay the bank - plus interest. As you repay a loan from your plan, the money you pay and interest goes straight back into your account. This means you're paying yourself the interest. |

|

|

|

|

|

|

Missed Opportunity for Growth

When you borrow from your savings, you're taking some of your money out of the market. Over time, your savings grows by taking advantage of market highs and riding out market lows. Taking a loan represents an opportunity cost, or the cost of missing out on the opportunity for potential growth in the market. |

|

|

Ultimately, it's best to leave your money in the account.

This approach has been shown to result in the greatest savings at retirement. Taking out money with a loan can put you at risk of not earning as much as if you had just left it alone – especially if you stop making contributions during the loan period. |

|

|

Paying more for the same investment.

Keep in mind, when you take a loan from your retirement plan account, you're selling shares of your investments. As you repay your loan the price of those shares might not be the same. You could pay a higher price to repurchase your shares, and therefore, receive fewer shares for your dollar. |

|

|

Other possible consequences

If you lose your job or decide to quit, you will probably have to repay the outstanding loan amount immediately, usually within 30 days. If you cannot repay the loan then the loan is viewed as a premature withdrawal. Income taxes will be assessed on the outstanding balance. You may also be subject to a 10% penalty and possible state penalties for early withdrawal. |

|

|

Even if you're still employed and can't pay back the loan, you may need to default on it - another case of premature withdrawal. The same taxes and penalties would apply.

|

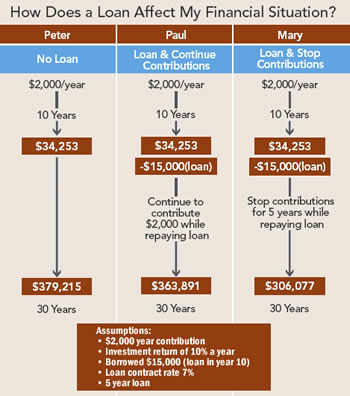

| Assumptions: |

|

|

|

|

Investment return of 10% a year |

|

|

Loan contract rate 7% |

|

|

5 year loan |

|

| Can You Get the Funds from Somewhere Else? |

| |

| Before you borrow from your retirement savings, consider other available alternatives and the costs of each option. |

|

| Examples include: |

|

|

|

Personal loans from a local bank. Banks have specific programs for school, medical expenses and other personal reasons. |

|

|

Mortgage loans. Available from both banks and mortgage companies. The competition among mortgage lenders has risen. First time home buyers in particular may be able to find special programs or loan packages. |

|

|

| |

|

|

|

|

Home equity loans. If you own a home, you may be able to get a line of credit using the equity in your home as collateral. Sometimes, an income tax deduction can apply with this type of loan. |

|

|

Support for tuition. There are many programs for paying school tuition, including loans through your school, and state and federal programs. Plus, there may be a tax deduction for interest paid on school loans. Also, your employer may offer a tuition reimbursement program. Remember - there are no scholarships for retirement. |

|

|

Decisions

Plan loan features provide you with flexibility and are a valuable benefit. However, before tapping your retirement account, check out your other options. Consider borrowing from your retirement savings only for a really important opportunity or emergency situation. |

|

Get Connected! Model a loan

|

|

| This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice. Where specific advice is necessary or appropriate, please consult with a qualified tax advisor, CPA, Financial Planner or Investment Manager. |

|

|

|