About Your Personal Rate of Return...

Personal rate of return is a person's own investment

performance based on his or her own transaction history and resulting cash

flows. This section outlines the standards and calculation methods for

determining your personal rate of return.

Time-Weighted

Rate of Return

Your personal rate of return was calculated using a

"time-weighted rate of return" method. Time-weighted rates of return take into account the amount of time an investor has been

invested in a certain security such as a stock or mutual fund. It measures how

well the investor performed in increasing the dollars that were invested and

provides a truer measurement of how investments have performed. Cash flows such

as contributions moving in and out of the investment(s) do not affect the

time-weighted rate of return. To be exact, your personal rate of return was

calculated using the time-weighted rate of return "Modified Dietz"

method where inflows and outflows are averaged for the entire period (no

monthly chaining).

Modified

Dietz Method Details...

When no cash flows are present, calculating total return is

accomplished for a given period using the following equation:

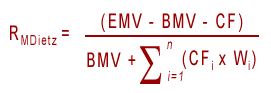

…where EMV is the market value of the asset at the end of

the period, including any accrued income. BMV is the market value of the asset

at the beginning of the period.

Time-weighted rate of return (TWRR) – Modified Dietz uses the beginning and

ending portfolio value for the month, and weights each

cash flow (contribution or withdrawal) by the amount of time it is invested.

The monthly portfolio returns are then geometrically linked to arrive at a

quarterly or annual return. The formula for estimating the time-weighted rate

of return using the Modified Dietz Method is…

…where EMV is the market value of the portfolio at the end

of the period, including all income accrued up to the end of the period, and

BMV is the portfolio's market value at the beginning of the period, including

all income accrued up to the end of the previous period. CF is the net cash

flows within the period where contributions to the portfolio are positive flows

or "inflows" and withdrawals or distributions are referred to as

negative flows or "outflows."

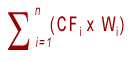

The equation above represents the sum of each cash flow CFi multiplied by its weight Wi. The weight Wi is

the proportion of the total number of days in the period that cash flow CFi has been held in (or out of) the portfolio. The

formula for Wi is…

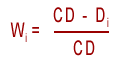

…where CD is the total number of calendar days in the

period and Di is the number of calendar days since the beginning of the

period in which cash flow CFi occurred. (The

numerator is based on the assumption that the cash

flows occur at the end of the day.) For example, if a cash flow occurred on

January 20th and if the month of January has 31 days, the ratio Wi is then

calculated as (31–20)/31 = 0.35483871.